The Appraisal, August 2024 — Is Home Insurance Broken?

Welcome to the August edition of The Appraisal, a newsletter on real estate tech. My writing focuses on the 30+ public companies operating at the intersection of real estate and technology. In this edition:

Real Estate Tech Index Performance Update

Thomvest x Keyway AI Adoption Survey

A Primer on the Home Insurance Market

Five Trending Topics

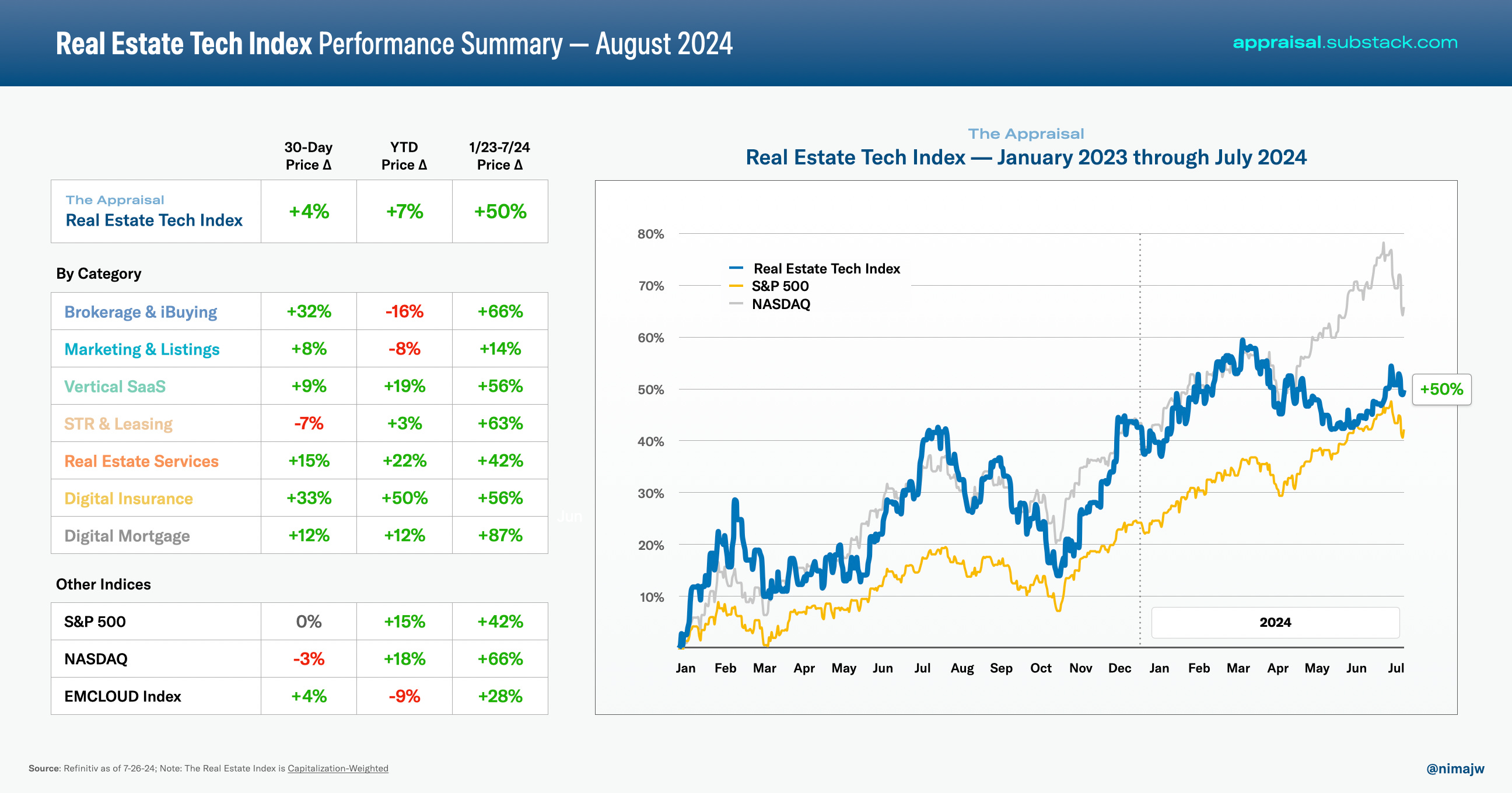

Real Estate Tech Index — August Update

The Real Estate Tech Index is up 7% year-to-date, down slightly from my last update. Recent inflation and unemployment data has buoyed expectations of rate cuts in September (a positive for the rate sensitive real estate sector, but may also be indicative of a broader slow down in the economy). However, softish earnings announcements from some of the larger companies in the Index have pulled down its overall performance for the year. Some examples:

Airbnb's first-quarter revenue rose 18% year-over-year to $2.14 billion. However, the company forecasted second-quarter revenue below Wall Street expectations, sending shares down 8% after the bell.

Opendoor’s outlook and forward commentary for Q3 disappointed investors as top-line guidance fell 18% below consensus estimates. The company expects to slow its home acquisition pace as it exercises prudence around striking a balance in its portfolio of homes and maintaining its clearance rates. Shares fell 14% following the earnings announcement.

Investors appear to be in a “wait and see” posture given ongoing uncertainty around interest rates, broader macro and an impending election. I don’t expect much movement across the Index until rate cuts do (finally) arrive and transition volume in the real estate sector picks up.

Thomvest x Keyway AI Adoption Survey

We just launched a survey with our friends at Keyway on AI adoption in the real estate industry. Our goal is to gain a better sense of receptiveness, trust, apprehensions, and desired outcomes through applied AI.

If you are a real estate investor, we’d love to hear your thoughts. The survey should take approximately 5-10 minutes to complete. Your participation and responses will be confidential and used solely for research purposes. Everyone who participates will receive a copy of the report.

Highlight of the Month — The Turbulent State of America's Property Insurance Market

Thanks to Sean Harper from Kin and Aaron Letzeiser from Obie for providing helpful commentary on the topic.

Rising home insurance premiums have been the subject of media attention recently, including good pieces from The New York Times and The Wall Street Journal. The numbers tell a stark story: net underwriting losses within the homeowners business line were about $15 billion in 2023, compared to $5.9 billion during the previous year. In an attempt to return to profitability, insurers have been boosting rates across the US: since 2019, the average cost of insuring a home has surged by more than 30%, far outpacing inflation (in some markets, premiums have more than doubled).

At the heart of this upheaval are four interconnected forces, each amplifying the others in a feedback loop that's exacerbating short-term volatility:

Climate Change and Extreme Weather — The increasing frequency and severity of natural disasters, from hurricanes to wildfires, are escalating risks and payouts for insurers.

Rising Replacement Costs — Inflation in construction materials and labor has significantly increased the cost of repairing or rebuilding damaged homes, leading to higher incurred losses for carriers.

Reinsurance Market Dynamics — Recent fluctuations in the global reinsurance market and a “hardening” in 2022 and 2023 are impacting insurers' ability to manage risk and set rates.

Regulatory Challenges — Varying state regulations create a patchwork of rules that can distort markets and affect insurers' willingness to offer coverage in certain areas. In markets where prices can freely adjust to balance supply and demand, consumers can still obtain insurance coverage (though at higher rates). Conversely, in regions where regulations hinder insurers from setting prices that accurately reflect rising costs, insurance availability tends to diminish (as in California).

Let's dive deeper into this perfect storm, exploring how these forces are reshaping the property insurance market and what it means for American homeowners.

1. Climate Change and Extreme Weather

Climate change is perhaps the most significant long-term driver of instability in the property insurance market. The increasing frequency and severity of extreme weather events are having profound impacts. According to the National Oceanic and Atmospheric Administration (NOAA), the U.S. experienced 28 separate billion-dollar weather and climate disasters in 2023, causing a total of $92.9 billion in damages.

These events are not evenly distributed across the country, leading to regional disparities in risk and insurance costs. Coastal areas face increasing risks from hurricanes and sea-level rise, while the Western United States is grappling with more frequent and severe wildfires. The Midwest is experiencing more intense flooding and severe storms.

Insurers are struggling to accurately price these evolving risks, often leading to either underpricing in high-risk areas or overpricing in lower-risk regions. This misalignment between risk and cost is creating market distortions and challenges for both insurers and homeowners.

2. Rising Replacement Costs

Inflationary impacts on labor and materials in the construction industry have become a critical factor in driving up insurance premiums nationwide. According to the National Association of Home Builders, construction material costs rose by 19.2% between 2021 and 2023, including:

Lumber prices spiked over 300% during the pandemic. Prices have stabilized but remain above pre-pandemic levels.

Steel mill product prices increased by 113% between 2020 and 2022.

Copper, essential for electrical wiring, saw a 94% price increase in the same period.

The impact on insurance is profound. When insurers calculate premiums, they're not just considering the likelihood of a disaster—they're factoring in the cost of rebuilding if the worst happens. As Sean Harper, founder & CEO of Kin, explains: “When you have a total loss and replacement costs are up 20% or 30%, that flows directly into the premium calculation.”

This dynamic creates a feedback loop: as replacement costs rise, insurers raise premiums to cover potential payouts. Higher premiums, in turn, make insurance less affordable, potentially leading to more uninsured or underinsured properties.

The situation is especially acute in disaster-prone areas. After Hurricane Ian in 2022, Florida saw reconstruction costs jump by 30-40% in some areas, driven by surging demand for materials and labor.

3. Reinsurance Market Dynamics

The reinsurance market, which provides insurance for insurance companies, plays a crucial role in the property insurance ecosystem. Recent years have seen significant volatility in this market:

The property catastrophe reinsurance rate-on-line index, which measures reinsurance pricing, increased by 13.2% in 2023, following a 14.8% increase in 2022.

Global reinsurance capital stood at $729 billion at the end of 2023, up from $652 billion in 2022, according to reinsurance broker Aon. However, this is still below the peak of $752 billion seen in 2020.

These fluctuations impact primary insurers' ability to manage risk and set rates. When reinsurance costs rise, primary insurers often pass these costs on to consumers in the form of higher premiums. If reinsurance becomes too expensive or unavailable for certain risks, primary insurers may choose to exit high-risk markets altogether.

The volatility in the reinsurance market is driven by several factors:

Increasing frequency and severity of natural disasters

Low interest rates reducing investment income for reinsurers

Global economic uncertainties affecting capital flows

One important trend worth highlighting is the growth of insurance-linked securities (ILS) as a source of reinsurance capital. ILS are financial instruments that transfer insurance risk to capital market investors. They provide an alternative source of capital for insurers and reinsurers, allowing them to transfer risks directly to investors rather than relying solely on traditional reinsurance. This has brought more investors into the reinsurance space, including pension funds, hedge funds, and sovereign wealth funds.

There has been an influx of capital into ILS over the last year, creating downward pressure on reinsurance pricing. The ILS market’s capital supply expanded by approximately $4 billion by the end of 2023, reaching an estimated total of $100 billion, according to AM Best.

So far in 2024, year-to-date issuance (January through June) has already exceeded all other years, with $11.9 billion in issuance according to Artemis. This has contributed to reinsurance rates falling by “mid- to high-single-digit” percentages in July, according to reinsurance broker Guy Carpenter.

4. Regulatory Challenges

The regulatory environment for property insurance varies significantly from state to state, producing a complex patchwork of rules and market conditions. The New York Times piece on home insurance does a nice job describing the dynamic this creates:

After big losses in those tightly regulated states, such as California, national insurers tend to raise rates in more loosely regulated states. In other words, homeowners in states with weaker rules may be overpaying for insurance, effectively subsidizing homeowners in states with tougher rules.

Two states that exemplify the challenges and different approaches to regulation are Florida and California.

Florida's property insurance market has been in crisis for years, driven by a combination of high hurricane risk, fraud, and litigation. The state has seen multiple insurer insolvencies and exits from the market. Citizens Property Insurance, the state-owned “insurer of last resort,” has grown to over 1.3 million policies as of May 2023 (up 42% in year-over-year), making the insurer one of the 10 largest homeowner underwriters in the country.

Fortunately, the state enacted recent policy changes designed to remove unnecessary costs from its system and encourage new carriers. Last year, legislators enacted reforms aimed at stabilizing the insurance market, including Senate Bill 2D which curtailed excessive litigation by restricting attorney fee multipliers, requiring proof of insurer breach before lawsuits, and preventing policyholders from transferring attorney fee rights to contractors. Additionally, the state increased funding for the "My Safe Florida Home" program to $200 million, expanding it to include condominiums and supporting home improvements that enhance hurricane resistance, which is expected to help reduce insurance premiums.

Prior to 2023, Florida was home to 9% of all homeowners policies, but 79% of all insurance-related lawsuits. The reforms have opened up opportunities for billions of reinsurance capital to flow into Florida's insurance market over the next 3-5 years, according to John Seo of Fermat Capital Management.

California is facing its own insurance crisis, particularly related to wildfire risk. Major insurers, including State Farm, have announced plans to stop writing new policies or non-renew existing ones. The California FAIR Plan, the state's insurer of last resort, has grown from 140,000 policies in 2018 to 373,000 in early 2024.

Aaron Letzeiser, co-founder of landlord insurance provider Obie, explained California's regulatory approach: “California, on the other hand, has almost the complete opposite problem in that the state legislature has capped the amount of increase that you can take on rate on a year over year basis.” This approach, while protecting consumers in the short term, has led to challenges for insurers trying to accurately price risk.

Legislators in California are trying to enact a number of changes to stabilize and future-proof its insurance market. The state’s insurance commissioner is proposing regulatory changes to allow insurance companies to use catastrophe models when setting rates for homeowners insurance, enabling them to account for future risks from events like wildfires. This is part of a broader initiative that also includes speeding up approval of rate increases and potentially allowing insurers to factor in reinsurance costs. The reforms aim to keep insurers operating in the state and address the worsening homeowner's insurance crisis.

The Road Ahead

As the property insurance market continues to evolve, several trends and potential solutions are emerging. Within each, technology will play an important role in driving better risk modeling, resiliency and efficiency.

Risk-Based Pricing: More accurate risk assessment and pricing could lead to better alignment between premiums and actual risk, potentially stabilizing markets but also resulting in higher costs for high-risk areas. This may impact affordability in the short term, but housing prices should ultimately adjust to reflect a total cost of ownership, inclusive of insurance premiums. Futureproof is building a climate-focused managing general agent (MGA) that factors climate-resilient structures into its pricing models. Kettle offers insurance and reinsurance for property owners in areas affected by catastrophic climate events.

Climate Adaptation and Damage Mitigation: Investment in resilience measures and climate change mitigation could reduce long-term risks and insurance costs. For example, Firemaps offers comprehensive wildfire defense solutions for homeowners in fire-prone areas. Eddy and Wint are focused on preventing water damage at properties

(water intrusion makes up 40% of all building-related issues).More Efficient Operations: Better-run insurance carriers will begin to win more share, and better technology is key to doing so. Insurtech companies like Kin have excelled by using technology to programmatically understand physical properties and price risk accordingly, more efficiently handle claims processing, and market directly to homeowners vs. via agents (whose commissions can range from 5-20% of premiums).

Thanks for reading! As always, please feel free to share feedback or thoughts on this post — you can respond to this email directly or shoot me a note at nima@thomvest.com.

Five Trending Topics

As I did last month, I’m sharing several great articles I’ve consumed recently that cover proptech, housing and the broader real estate market. Going forward, I’ll try to share at least a handful of links in each newsletter.

Landlords Used Software to Set Rents. Then Came the Lawsuits. [New York Times] Details on the lawsuit against RealPage, whose software allegedly allows landlords to share rental pricing data and collaborate to raise rents, potentially violating antitrust laws. Multiple tenants, prosecutors, and government agencies are challenging this practice, claiming it artificially inflates rental prices in various cities across the United States.

Building Materials — Part 1 [Scuttleblurb] Excellent deep dive on the building materials industry. The first post focuses on BlueLinx, a major two-step distributor. It explores the company's history, business model, and recent performance, while also examining broader industry trends, challenges, and the impact of economic cycles and commodity price fluctuations on profitability in the building materials sector.

Renting Forever and Trying to Create a Strong Financial Future [New York Times] Good piece exploring the growing trend of people choosing to rent homes long-term rather than buy, driven by rising housing costs and interest rates. It discusses strategies for building wealth without homeownership, including aggressive investing and financial planning, while highlighting both the challenges and potential benefits of a renting lifestyle. Interesting to think through the longer-term implications for real estate firms, technology companies, and cities if this trend persists.

KKR Makes Its Biggest Foray Into Apartments, Betting on Rising Rents [Wall Street Journal] KKR recently completed its largest-ever apartment building purchase for $2.1 billion, acquiring over 5,200 units across the US. This deal, along with other recent large acquisitions by firms like Blackstone and Brookfield, suggests growing investor confidence in future rent and value increases for apartments, particularly as construction starts decline and rents begin to rise in some regions.

VP Harris Announces First-of-Its-Kind Funding to Lower Housing Costs by Reducing Barriers to Building More Homes [White House] This initiative is part of the Biden-Harris Administration's broader efforts to increase housing supply and affordability, with additional funding and measures planned to support housing development and accessibility nationwide. I share this as an example of the actions that can and should be taken at the federal level to encourage housing supply; despite recent progress, the country still faces a supply deficit of several million homes.

Note: Charts and graphs provided within are for informational purposes solely and should not be relied upon when making any investment decision. The content speaks only as of the date indicated. Any projections, estimates, forecasts, targets, prospects, and/or opinions expressed in these materials are subject to change without notice and may differ or be contrary to opinions expressed by others.