The Appraisal, April 2024 — What's Interesting in Real Estate Tech? 🧐

Welcome to the April edition of The Appraisal, a newsletter on real estate tech. My writing focuses on the 30+ public companies operating at the intersection of real estate and technology. In this edition, we’ll review the Real Estate Tech Index’s recent performance and highlight a few compelling investment themes for 2024 I’m excited about.

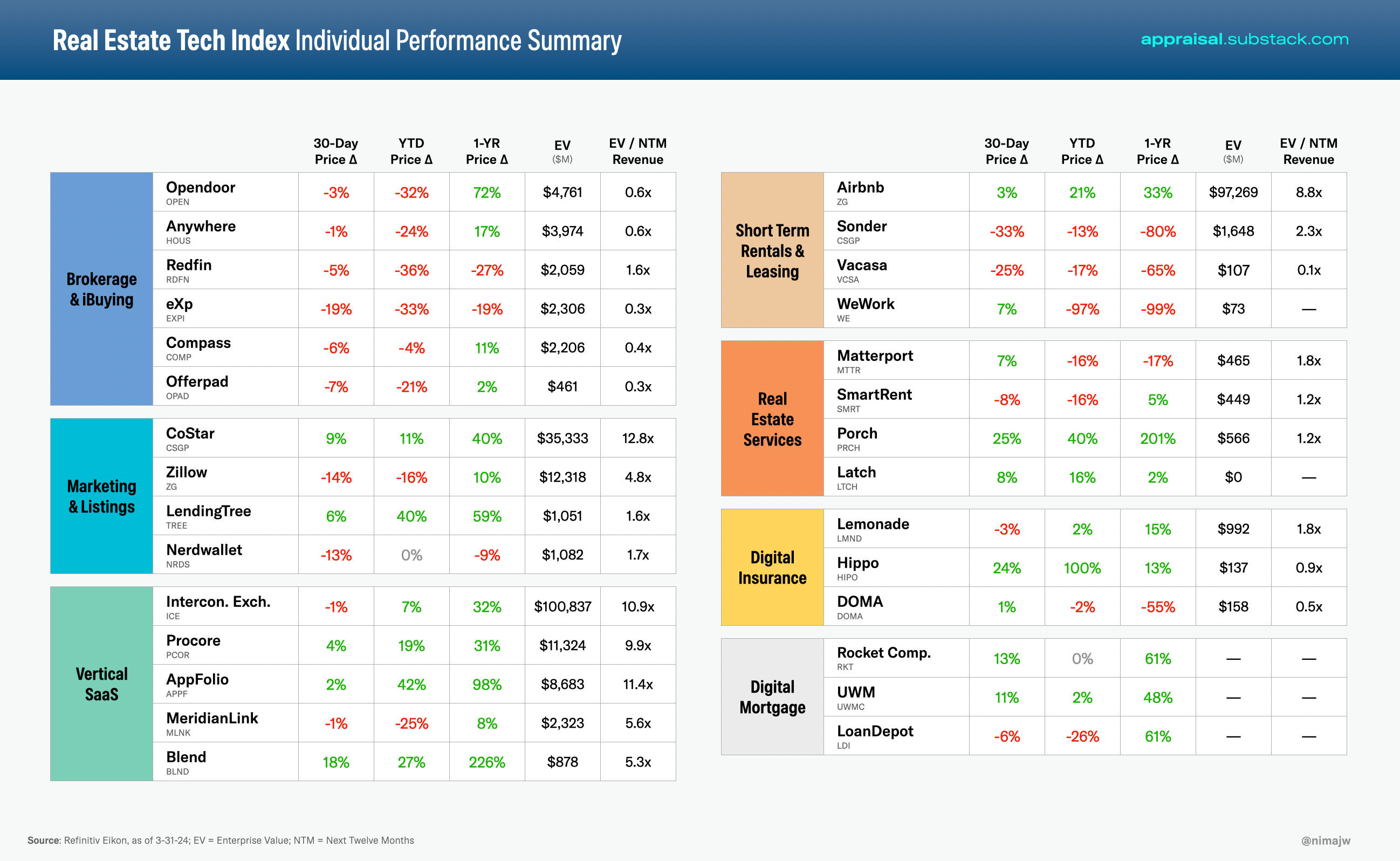

The Index is up 11% through the first quarter of 2024. You’ll see that the “Brokerage & iBuying” segment is the outlier, down 26% through Q1. We can point to the recent NAR settlement to understand why — uncertainty around its long-term implications have driven brokerage stocks down. This is an area we will actively track, so expect more content on this topic in future newsletters.

In other proptech news — CoStar announced its acquisition of Matterport earlier this week. Good to see two companies in the Index coming together in what may be the start of a consolidation wave in the sector. The transaction values Matterport at $5.50 per share, implying an equity value of approximately $2.1 billion. This represents a healthy 216% premium to Friday's close price of $1.74. Scroll to the bottom of this post for more charts and detail on the Index’s performance.

If you have any colleagues that may find The Appraisal valuable, please feel free to share this newsletter. Thank you!

Highlight of the Month — Investment Themes for 2024

It’s a unique time to be investing in real estate technology startups. Rising interest rates, and the downstream impact on transaction activity and software spend have created headwinds for many venture-backed startups in the category. This has resulted in dampened investment activity over the last 18 months — venture dollars flowing into real estate technology startups declined 62% year-over-year in 2023.

Against this backdrop, it’s important to think critically about the idea spaces in real estate that remain unexplored. Where is there room for software adoption, what new use cases do LLMs enable, and are there still opportunities for venture-scale outcomes in real estate?

A bright spot in the venture data is the seed market — the number of seed financings last year was in-line with 2021 (90 and 92 deals, respectively). This activity at the earliest stages speaks to sustained investor excitement about what’s possible in real estate, particularly as AI-enabled use cases emerge. For the pollyannish amongst us, the investment setup is actually quite compelling — declining venture activity (and valuations) coupled with an accelerating pace of innovation.

So where am I focused on investing in 2024? I’ve detailed a few initial areas I’m spending time in this year — this list is ever-evolving and I welcome feedback from the startup and venture communities.

1. “Control Point” Software Businesses in Real Estate

Vertical software companies have proliferated over the last decade. Across real estate and construction, there are specialized products for roofers, commercial kitchen operators, pool service companies, flooring retailers, and many more.

Venture firm Tidemark has published a great series of posts on how vertical software businesses can reach venture-scale (loosely defined as scaling to $100m+ ARR). Core to their investment strategy is identifying control point businesses, defined as “the most important system, the last to be thrown out before an owner ceases operations.” Importance is a byproduct of three primary attributes: Workflow (the system other systems integrate into), Data (system that creates and holds the most critical information), and Account (system is used by key employees at the company).

Control point businesses tend to include CRM-like functionality in the front-office and accounting or ERP systems in the back-office. They are core to how businesses run and are often very difficult to displace (just last week American food processing company Lamb Weston reported over $135 million in lost revenue due to a buggy ERP transition).

In real estate, the property management system (PMS) has long been the primary control point for most firms. There are several PMS vendors — Entrata, AppFolio, Yardi, MRI & RealPage — that have reached $100m+ ARR scale (AppFolio is the sole public company in this list, valued at nearly $9B). They are the platforms that firms rely on as their primary system of record, and they’re very sticky as a result — despite low NPS scores and frequent customer complaints. They’ve also expanded their platforms (often via M&A) to pull in multiple use cases — tenant screening, revenue management, asset management, and more.

So do new entrants stand a chance? There are three interesting control point wedges worth exploring:

Wedge 1 — Target “greenfield” customer segments

Real estate has historically been a difficult vertical to sell into — high customer fragmentation, buyers lack software budgets, generally lethargy around technology adoption, etc. And startups need to overcome the distribution advantages legacy systems like PMSs have built over decades.

Fortunately, new approaches to monetization and new product experiences (enabled in part by LLMs) are unlocking “untouched” market segments that don’t have existing control point systems in place. A couple of examples:

Baselane (a Thomvest portfolio company) targets independent landlords that have historically been difficult to acquire and monetize. The big unlock in their business comes from bundling operating tools like rent collection and tenant screening with banking functionality. In doing so, they become the primary control point for independent landlords, providing ample opportunity to monetize via payments, insurance lending and premium features.

ServiceTitan has scaled by to nearly $500m ARR by building vertical software for the roughly 2.5 million home service companies in the U.S. In the past, many home services SMBs relied on pen and paper or spreadsheets to manage operations and customers. ServiceTitan has built an all-in-one platform for managing payments, accounting, scheduling, marketing, payroll and more — in doing so, they’ve become the primary control point for thousands of long-tail SMBs.

Wedge 2 — Wrap around the control point

In cases where there is an existing control point in place, high switching costs and general inertia may make it challenging for new startups to compete. In lieu of replacing systems, can these startups build value around the control point? And in doing so, can they shift user activity to their platforms (i.e. become the “system of engagement”)? We’ve seen this happen in other sectors — for example, our portfolio company Clari built sales forecasting and analytics on top of Salesforce — functionality the CRM didn’t offer. Gong is another relevant example in the sales tech space.

Startups that have the best shot of scaling as a control point compliment tend to have the following attributes:

New data — companies must access or analyze data that provides value beyond what can be accomplished in the existing control point system. For example, products like OpenSpace and OnsiteIQ have become essential platforms for contractors and developers by capturing digital images and videos on construction sites. This puts them in a unique position as a critical project tracking and analytics platforms. Two great examples of products that sits alongside the primary control point (usually Procore) by creating unique, differentiated value. Another example: Convex (which was recently acquired by ServiceTitan) has built valuable lead enrichment and sales engagement functionality on top of CRMs used by subcontractors.

New communication and workflow tools — startups can create value alongside the control point by making their customers more efficient. This usually means workflow automation. For example, Forge and Factor streamline communication with suppliers, order tracking, purchase approvals and more for their customers (which are primarily hardware manufacturers). They do so by integrating deeply with a customer’s ERP system. In real estate, Haven is building LLM-powered communication tools for tenants and real estate owners.

Wedge 3 — “Sell work not software”

Sarah Tavel from Benchmark has a great post on startup opportunities enabled by LLMs. In the post, she encourages companies to complete entire tasks or processes for customers, rather than simply offering incremental software tools:

While there are fantastic startups innovating to improve employee productivity, LLMs create an opportunity for startups to look beyond this way of thinking and discover surface area that previously was out of bounds for selling software given the required GTM and pricing limitations of software. To do this, rather than sell software to improve an end-user's productivity, founders should consider what it would look like to sell the work itself. Selling work opens up new vertical opportunities that wouldn’t have otherwise supported a software company.

I believe this is especially true in real estate. Companies in this sector are more accustomed to hiring service providers (for example, third-party property management) than they are buying software. In these instances, the service provider becomes the decision maker when selecting control point software. This creates an interesting opportunity to become the control point while selling on terms a real estate buyer understands and values. And there are many labor-intensive or manual workflows that are ripe for automation. Pilot has done a nice job of this in the accounting space.

While “tech-enabled services” aren’t a new concept, generative AI may enable a new level of automation and scale — selling a service while enjoying software-like gross margins and growth rates. We are beginning to see this play out in other industries; for example, EvenUp creates demand packages for personal injury law firms, replacing time consuming and manual work typically completed by paralegals.

In the mortgage space, Maxwell (another Thomvest portfolio company) has built an AI-enabled “mortgage fulfillment-as-a-service” offering. Selling the work is particularly salient in mortgage, where cyclicality leads to constant periods of understaffing and overstaffing. Maxwell helps mortgage companies shift their overhead expense from from a fixed to a variable cost while also delivering a more consistent, higher-quality work product. APM Help and Rexera are also good examples of selling the work (in this case property accounting and HOA documents acquisition) in the real estate vertical.

I expect to see a wave of sell the work companies in real estate over the next year, so please reach out if you are working on something here.

2. AI’s Impact on Construction Productivity

Over the last five decades, construction labor productivity has declined on an absolute basis — today a construction worker is less productive than their 1950 equivalent. We can attribute this to a number of factors: heightened safety standards, increasing building complexity and skilled labor shortages. We’ve long talked about the role technology may play in improving the construction process, but we’ve yet to see it at scale in the field. Some view new technologies as a doubled-edged sword — for instance, mobile phone adoption has enabled better collaboration on job sites, but has also become “a huge safety liability” and “a dangerous distraction” according to general contractors.

Will the promise of AI finally make a dent in how productively we build buildings? So far, some of the more interesting startups I’ve come across are focused on the “soft costs” component of real estate development (design, entitlement, financing, etc.) — which can represent 30%+ of total project costs. It makes sense — this is typically labor intensive “white-collar” work completed in offices not job sites, a prime candidate for generative AI tools. A few areas where I’ve seen interesting startups emerge:

Pre-development — companies like TestFit and Cedar allow for rapid analysis of development feasibility based on parcel size, zoning overlay, cost and other factors. Companies like PermitFlow and Pulley are automating the permitting and entitlement process.

Pre-construction — companies like Drawer and Togal are extracting insights from construction drawings, enabling GCs to “automatically detect, measure, compare and label project spaces and features on architectural plans and drawings in seconds, not hours.”

Design — companies like Integrated Projects, Tailorbird, and Acelab are shortening the design cycle for architects and designers. I also see an emerging opportunity to build lightweight design tools used by non-designers (analogous to Canva’s efforts in graphic design).

On the construction site, there is also growing excitement about how AI can also transform physical robots by giving them the ability to recognize objects and respond to human commands about those objects. We are in the very early days here, but there has been a flurry of startup formation and funding to build trade-specific robots (for example, robots for drywall finishing, commercial landscaping, drawing layout lines, and masonry).

3. Residential Real Estate in a Post-NAR World

Redfin’s CEO Glenn Kelman described the NAR settlement as an “astroid hitting the industry.” Uncertainty abounds with regards to the settlement, its implications for realtors and its impact on the home buying experience. In the (likely) event that buy-side agent commissions are reduced, I expect lower-producing agents to leave the industry (during the height of the COVID-era home buying frenzy, there were more agents than homes for sale).

Agents that remain in the industry will seek measures to become more efficient (e.g., by leveraging tech vendors to better scale operations and marketing). And the traditional brokerage model simply won’t “pencil” any longer — the model requires a cost load that won’t be offset by declining commissions.

This may create meaningful headwinds for existing real estate companies (and interesting opportunities for new entrants). For example, Morgan Stanley recently commented on settlement’s potential impact on Zillow and Compass:

We see a potential bear case where lower commissions cause brokers to reduce their marketing spend on Z, as we estimate that for every 10bp reduction in commission rates, Z could see 7% downside to ’25 EBITDA.

We see the impact from any potential commission reductions as a relatively clear negative for COMP. For every 10bp reduction in commission rates, we estimate that COMP would see 19% downside to its ’25 EBITDA.

Over time, the settlement should create healthy competition and innovation within the home buying category. It will force parties to earn the right to their commissions by delivering more value per transaction. I think this will be done in a couple of ways:

Models that bundle several aspects of a real estate transaction (such as mortgage, title and agent representation) in a RESPA-compliant manner.

Changes to the home shopping experience — more self-service home viewing with agents available on-demand for advice, market intelligence, negotiation and diligence services. Better alignment of costs with specific services provided.

Thanks for reading! As always, please feel free to share feedback or thoughts on this newsletter — you can respond to this email directly or shoot me a note at nima@thomvest.com.

Five Trending Topics

As I did last month, I’m sharing several great articles I’ve consumed recently that cover proptech, housing and the broader real estate market. Going forward, I’ll try to share at least a handful of links in each newsletter.

Once America’s Hottest Housing Market, Austin Is Running in Reverse [Wall Street Journal] The Austin, Texas housing market, which boomed during the pandemic due to an influx of remote workers and businesses, is now leading the nation in declining home prices and apartment rents due to overbuilding and slowing population growth, despite the city's job growth remaining above the national average. While this may create challenges for homeowners who bought at the height of the market, this is in many ways an encouraging development in a market that can respond to changes in demand (both from a land supply and entitlement perspective) by building more homes to meet that demand. This leads to supply gluts in some instances, but also preserves affordability.

America’s Affordable Housing Crisis [New York Times] Good article discussing how rising housing costs are a major problem across the United States, and how Democrats and Republicans in various states are actually working together to pass legislation that removes barriers to new construction and increases housing density, in an effort to make housing more affordable. From the article: “Already, Democrats and Republicans in Montana and Arizona have united for housing legislation. A similar coalition has taken shape in other states, including Texas, Minnesota and North Carolina. Even in California and Oregon, whose governments are dominated by Democrats, Republican votes have helped pass housing bills.”

NAR Settlement: Kaboom! [Redfin Blog] Good perspective from Redfin’s founder and CEO Glenn Kelman, who has not been bashful about his issues with the NAR (Redfin resigned from the NAR last year). In this post, Kelman shares some thoughts on the settlement’s potential implications for home buyers and sellers. The settlement introduces a major structural change by eliminating certain commission listing practices, potentially leading to more transparent agent hiring and fee negotiations, though the impact on industry cooperation remains uncertain.

Unfreezing Housing: What Biden’s Plan Would Mean For Affordability [Forbes] Discusses the Biden administration's ambitious plan to build 500,000 starter homes as a response to the affordable housing crisis, reflecting the administration's broader efforts to address housing affordability and accessibility in the U.S.

Inside a Chinese Ghost Town of Abandoned Mansions [Wall Street Journal] A fun video from WSJ visiting an abandoned “ghost town” in Shenyang City built by the Greenland Group to explain how China’s real-estate slump has become a headache for the government. Really striking to visualize the breadth of construction that has gone unused.

Additional Index Performance Charts

Note: Charts and graphs provided within are for informational purposes solely and should not be relied upon when making any investment decision. The content speaks only as of the date indicated. Any projections, estimates, forecasts, targets, prospects, and/or opinions expressed in these materials are subject to change without notice and may differ or be contrary to opinions expressed by others.

Great post on Control point software. The significance here is why the base building system OEMs are making acquisitions - JCI bought FM Systems, Trane bought Nuvolo, and Siemens bought Brightly (formerly Dude Solutions).