The Appraisal, October 2022 — Real Estate Tech Market Map, Multiples Update

The Appraisal, October 2022 — Real Estate Tech Market Map, Multiples Update

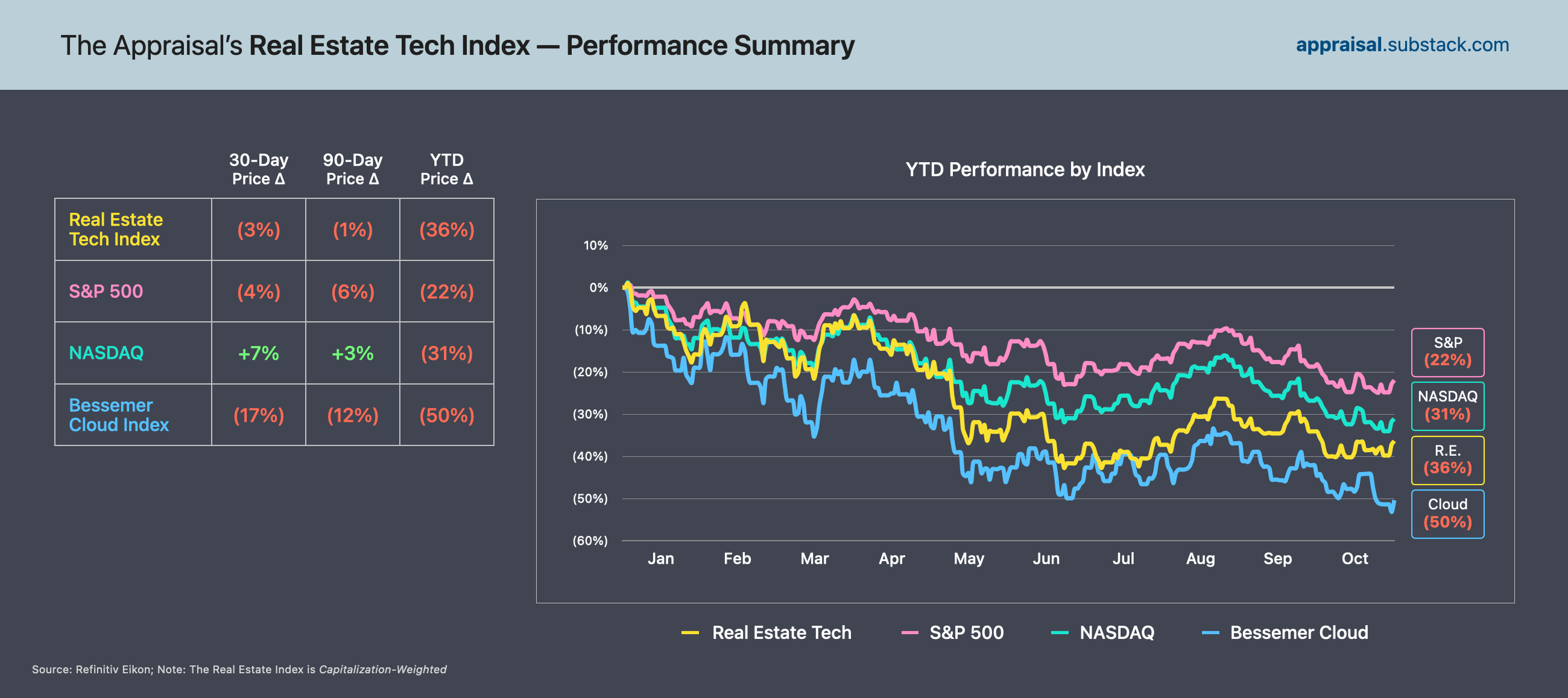

The Appraisal's Index is designed to track the performance of emerging, publicly traded real estate technology companies.

Welcome to the second edition of The Appraisal, a monthly newsletter on real estate tech. My writing focuses on the 30+ public companies operating at the intersection of real estate and technology. The Real Estate Tech Index experienced further declines this month and is down 36% year-to-date. This contraction is part of broader market sell-offs across every major index — the S&P 500 and NASDAQ are down 22% and 31% YTD, respectively.

Rising interest rates are an obvious culprit for today’s bear market, particularly for companies operating in the real estate sector. The speed and level to which rates have climbed this year have greatly reduced refinance activity and exacerbated existing affordability challenges in the purchase market. The average 30-year fixed mortgage rate hit 6.94% this week — the highest level since 2002. Residential housing activity ranging from new housing starts to home sales have been on downward trends coinciding with the rise in rates. Purchase and refinance applications are down 38% and 86% over the year, respectively. Redfin reported a drop in new listing volume in September of 22%—the largest decline since April 2020 when the onset of the pandemic brought the housing market to a near halt.

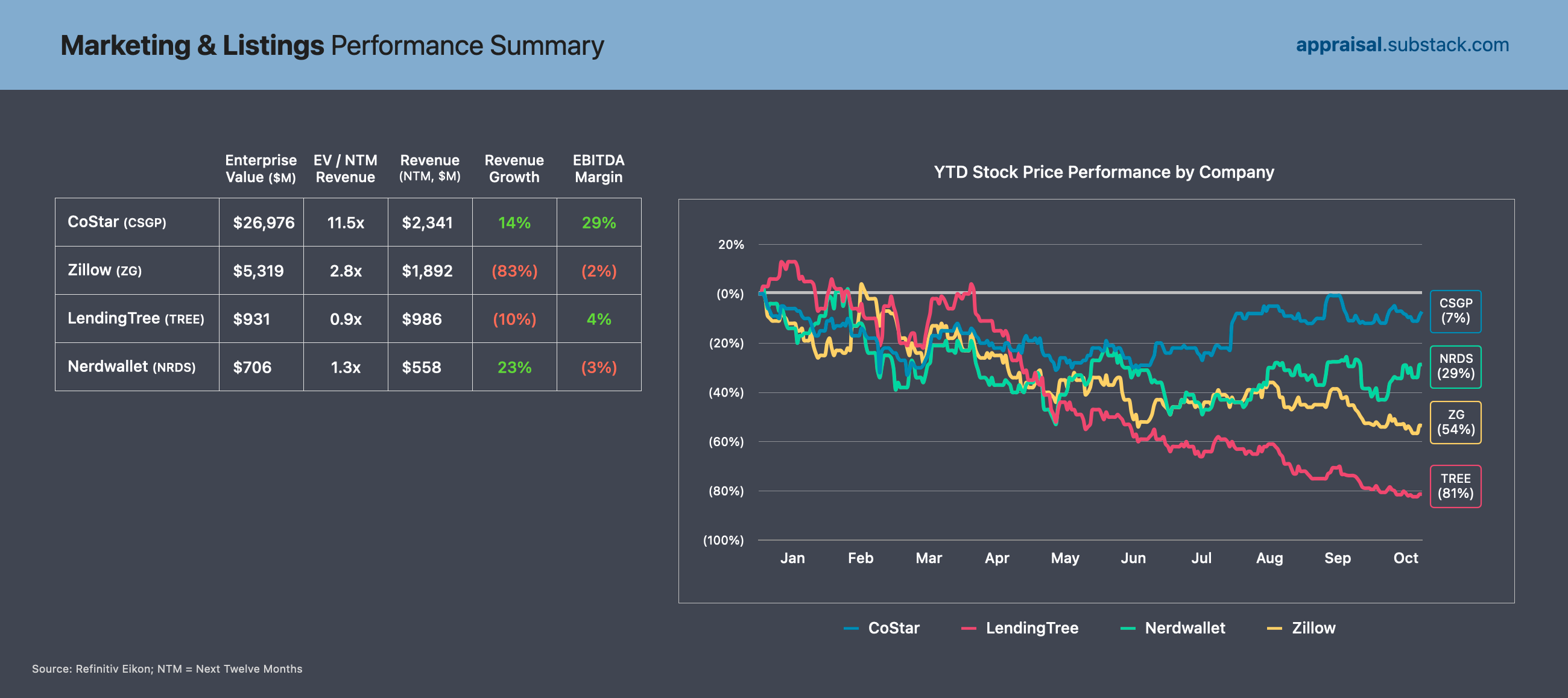

With slowing transaction activity and looming recessionary fears, many public real estate technology companies have traded down meaningfully this year, including Zillow (-54%), Compass (-70%), Opendoor (-83%) and Redfin (-89%). Unfortunately, with inflation still rampant, the Federal Reserve will likely continue raising interest rates. That means we may not see high mortgage rates—a primary driver of housing demand—decline until early to mid-2023.

As a result, nearly every company in the real estate index has announced layoffs or hiring freezes in an effort to control cash burn over the short term. A few examples:

In September, Hippo released its 2022 Investor Day presentation which details the company’s path to EBITDA profitability by Q4 2024. Unfortunately these plans do not seem to have resonated with public investors — Hippo has traded down more than 40% since their Investor Day and the company announced a 1-to-25 reverse stock split last month.

Compass announced plans to cut its expenses by $320 million this year in an effort to assuage investors. This included a lay off impacting roughly 50% of the company’s 1,500-person technology team.

Sonder, a short-term rental platform, announced a corporate restructuring in June in an effort to cut cash costs by $85 million annually. The company’s stated goal is to reach positive free cash flow in 2023 (see Sonder’s most recent investor presentation for more detail).

The next several months will be quite interesting for these companies: public investors will certainly monitor the macroeconomic environment (CPI, rate hikes, geopolitical risk, etc.) and its impact on real estate. More importantly, however, they will track whether leadership teams can successfully steer their companies towards positive cash flow despite choppy market conditions. With Q3 earnings season around the corner we should have early data on this transition shortly.

If you have any colleagues may find The Appraisal valuable, please feel free to share this newsletter. Thank you and enjoy!

Highlight of the Month — The 2022 Real Estate Tech Market Map

I recently published my 2022 real estate tech market map on the Thomvest blog, which includes more than 275 companies operating within the residential real estate segment. Assembling this map is a labor of love that keeps me up-to-speed on the dizzying pace of company formation in the category (this year’s map included more than 70 new startups). In the blog post I got into detail on two sub-areas in the map that I’m particularly excited about:

New core infrastructure in mortgage, from borrower acquisition to servicing: The mortgage industry has faced several headwinds this year — rising interest rates, limited housing supply, and record-high home prices impacting affordability. To survive, lenders must do more with less resources, and they will turn to technology partners that enable automation, delight customers and drive down cost. I recently wrote about Thomvest’s investment in Willow Servicing, which fits directly into this thesis.

The rise of “indie” real estate investors, enabled by new ownership models: I added new category to the map this year, “Rental Investment Platforms,” which represents the many startups enabling individual investors to invest in real estate. These platforms lower the barriers to entry for investing in real estate. And collectively, they offer several distinct “flavors” for ownership — from fractional, passive investing opportunities (Arrived, Lofty), to single-asset purchases (Roofstock, Doorvest), to real estate fund investments (Fundrise, Keyway).

Head over to the Thomvest blog for the full post, and look out for my commercial real estate tech map, which is arriving next month. On to the multiples update…

Public Real Estate Tech Performance Summaries

Below I’ve included category-level performance summaries. I will update the charts included in this newsletter on a monthly basis in order to track company & category performance over time. I am always open to feedback or thoughts on the newsletter — please feel free to respond to this email or shoot me a note at nima@thomvest.com.

Note: Charts and graphs provided within are for informational purposes solely and should not be relied upon when making any investment decision. The content speaks only as of the date indicated. Any projections, estimates, forecasts, targets, prospects, and/or opinions expressed in these materials are subject to change without notice and may differ or be contrary to opinions expressed by others.