The Appraisal, December 2022 — Housing Report, Q3 Earnings Update

Happy holidays! Welcome to the third edition of The Appraisal, a monthly newsletter on real estate tech. My writing focuses on the 30+ public companies operating at the intersection of real estate and technology. The Real Estate Tech Index is down 42% year-to-date. This contraction is part of broader declines across every major index — the S&P 500 and NASDAQ are down 20% and 33% YTD, respectively.

Many companies are trading at a fraction of their IPO value, some are even trading at a negative enterprise value (market cap is less than net cash on hand). As we close out the year, many investors continue to have questions around the long-term prospects of these businesses, particularly during a period of macroeconomic uncertainty and interest rate volatility.

Since my last newsletter, nearly every company in the index has reported its Q3 earnings. While earnings were mixed overall, there were some interesting results worth highlighting. In particular, management teams are laser focused on reaching profitability over the next several quarters, and Q3 earnings gave us a glimpse at how companies are progressing towards that goal:

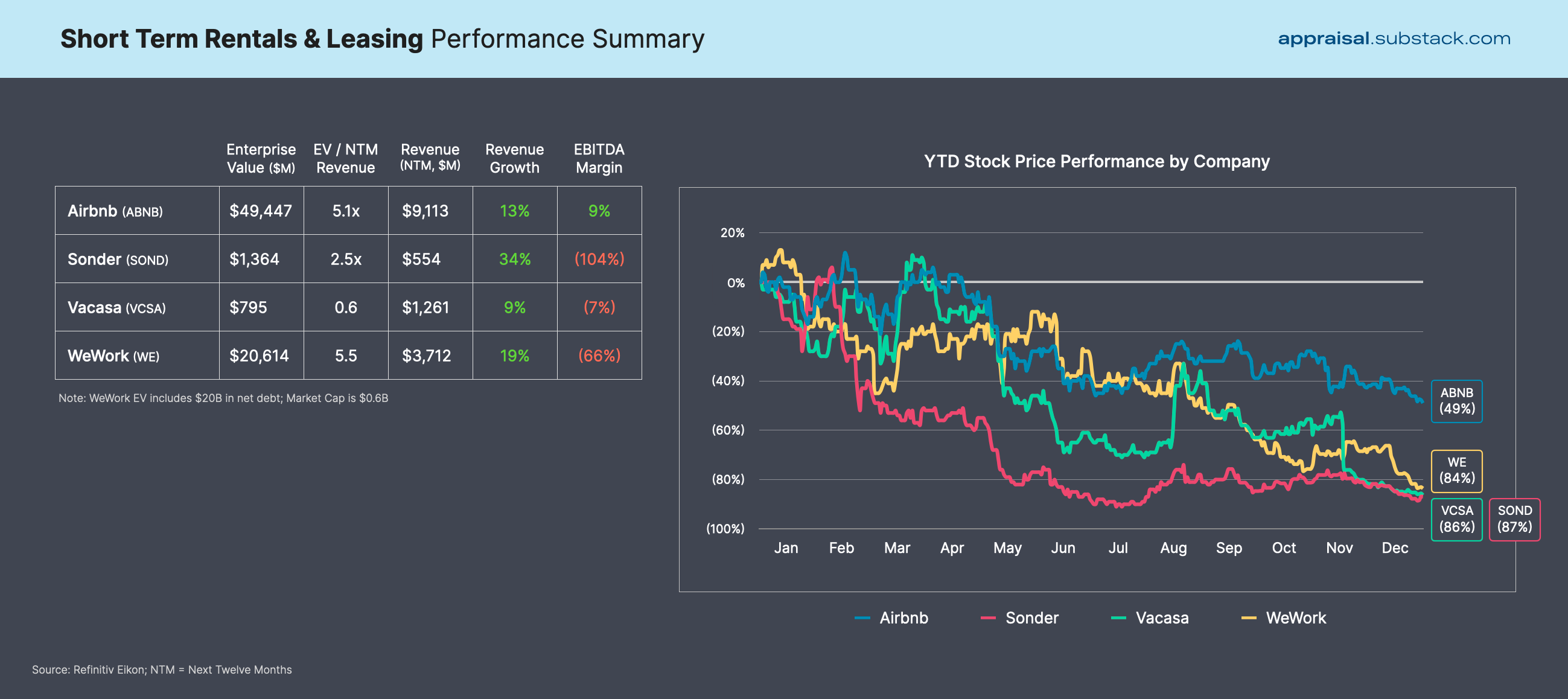

WeWork (WE) — Revenue grew 24% year-over-year in Q3, but the company missed net income expectations (WE posted a loss of 75 cents per share vs. an expected 48 cents per share). WE is down more than 50% since its Q3 earnings announcement in November. WeWork’s management team emphasized its focus on reaching profitability — recent actions include a planned closure of 140 underperforming locations, an extension of its $1.25B senior debt facility from February 2024 to March 2025, and a renegotiation of more than 480 lease agreements. The company has cut burn in half since last year — WE’s free cash flow was ($205M) in Q3 2022 vs. ($441M) in Q3 2021. The company has access to about $1.4B in liquidity (cash and secured notes), so it will need to act swiftly in its quest for profitability. Interestingly, analysts remain optimistic about the company’s prospects in 2023 — the median price target is $7.75, a 5x+ premium to today’s stock price.

Opendoor (OPEN) — Revenue of $3.36B came in above consensus of $2.64B, but its operating loss of $(810M) missed analyst expectations of $(226M), due in part to a $573M valuation adjustment on writing down homes in inventory. Shortly after its Q3 earnings release, Opendoor announced that CFO Carrie Wheeler will be taking on the role of CEO, with co-founder and CEO Eric Wu transitioning to his new role as President, Marketplace. In many ways, this transition makes sense as OPEN remains focused on selling down the old book of homes and optimizing the cost structure in the short term. Over the long term, Wu will work to transition the business to a more asset-light marketplace model — for example, Opendoor recently launched Exclusives Listings which allows buyers and sellers to transact directly on the platform, and partnered with Zillow to surface cash offers within the Zillow app.

Doma (DOMA) — Q3 retained premium and fees were $43M, down 40% year-over-year and ~19% below analyst estimates. The housing market and interest rate environment have meaningfully impacted the stock, which is down more than 92% this year. Doma’s management team is also banging the “path to profitability” drum. Despite the tough year, the company remains optimistic: “Doma is now committed to accelerating its path to profitability and achieving positive adjusted EBITDA earlier in 2023 than previously communicated.” To do so, the company must aggressively drive down its cost structure (it has an extensive local retail footprint) while pivoting to the purchase market (prior growth was largely fueled by refinancings) and improving gross margin. Doma’s net cash is $83M and it forecasts reducing headcount costs by more than half next year, so there appears to be sufficient runway to navigate a business transition during a potentially choppy mortgage market in 2023.

If you have any colleagues may find The Appraisal valuable, please feel free to share this newsletter. Thank you and enjoy!

Highlight of the Month — The Thomvest Housing Market Report

Last week I released an update to the Thomvest Housing Report, which includes market data through Q3 2022. It’s been a dizzying two years in the U.S. housing market — 2021 was arguably the hottest year on record for residential real estate, driven by pandemic-related fiscal stimulus and historically low interest rates. In 2022, the Federal Reserve reversed course and began aggressively hiking interest rates in an effort to cool inflation and home price appreciation. Heading into 2023, many fear that we are headed towards a severe housing correction. Fannie Mae forecasts $1.7T in total mortgage originations and and 3.9M existing home sales in 2023, down 26% and 23% year-over-year, respectively.

Many over-heated markets are already experiencing a correction (i.e. Boise, ID & Austin, TX). However, as I detail in the report, there are many supply and demand drivers that may moderate broader home price declines in 2023, including:

Supply headwinds: Currently there are only 3.3 million homes for sale in the US, according to the National Association of Realtors, a multi-decade low. Two-thirds of homeowners have mortgage rates under 4%, so there is a strong disincentive to sell and buy another home. Additionally, home builders are backing off starting on new home construction as they continue to try to offload the homes they’ve already built. Finally, mortgage delinquency rates are near historic lows, suggesting that we may not experience a foreclosure wave that expands housing supply and drives down pricing (as we experienced in 2008).

Demand tailwinds: While mortgage rates more than doubled in 2022, rates hit a three-month low last week, and many forecasters project that rates will drop below 6% in 2023. Additionally, demographic data suggests that the universe of first-time homebuyers (median age of 33) over the next 24 months will be the largest it has been in 30+ years. Remote work has also enabled migration to new markets that have historically not experienced meaningful demand shocks (see Nashville, TN & Raleigh, NC). Finally, institutional investors have earmarked up to $110 billion to purchase or build single-family rentals, according to Zelman & Associates.

It will be certainly interesting to monitor how the housing market evolves in 2023 and how management teams navigate this period of volatility. Investors will track the macroeconomic environment (CPI, rate hikes, geopolitical risk, etc.) and its impact on the real estate sector and the many companies operating within the housing market.

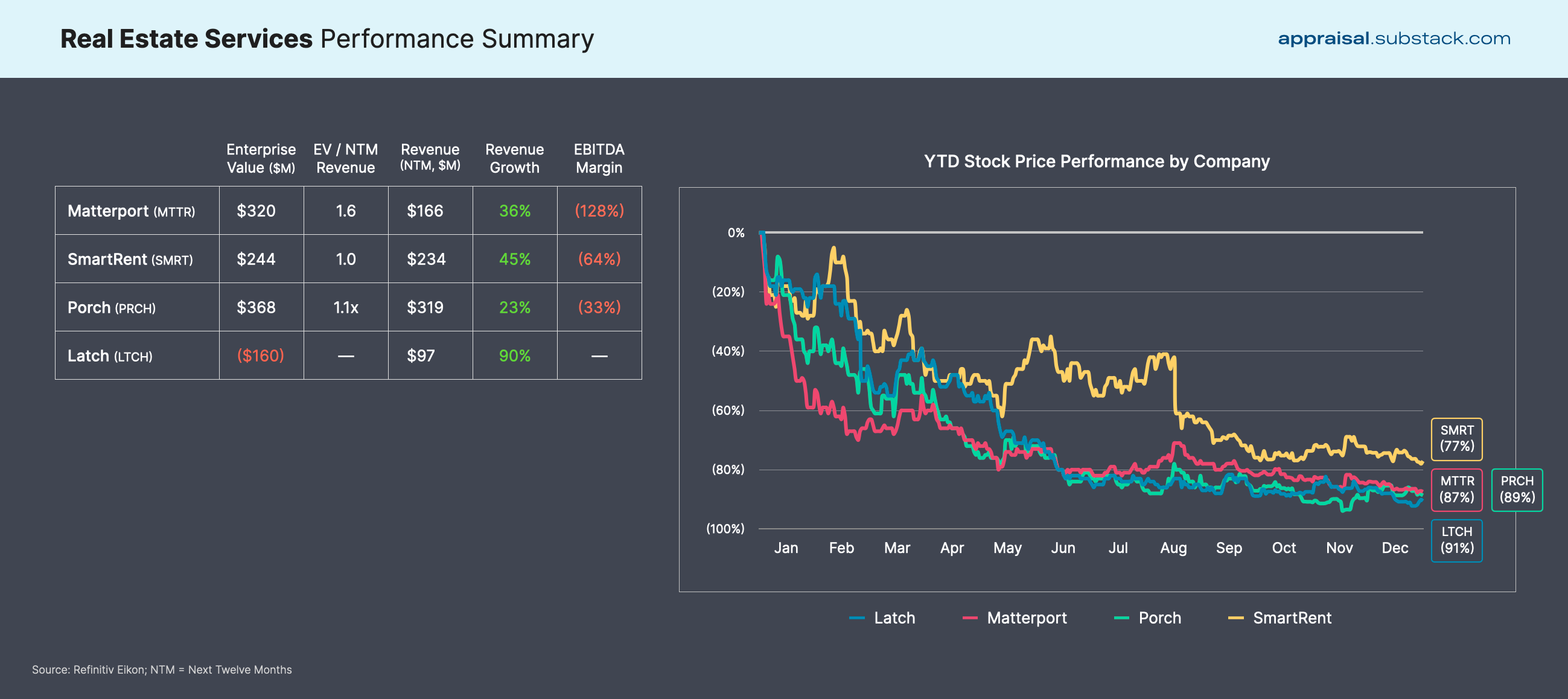

Public Real Estate Tech Performance Summaries

Below I’ve included category-level performance summaries. I will update the charts included in this newsletter on a monthly basis in order to track company & category performance over time. I am always open to feedback or thoughts on the newsletter — please feel free to respond to this email or shoot me a note at nima@thomvest.com.

Note: Charts and graphs provided within are for informational purposes solely and should not be relied upon when making any investment decision. The content speaks only as of the date indicated. Any projections, estimates, forecasts, targets, prospects, and/or opinions expressed in these materials are subject to change without notice and may differ or be contrary to opinions expressed by others.