The Appraisal, August 2022 — The Inaugural Edition

The Appraisal's Index is designed to track the performance of emerging, publicly traded real estate technology companies.

Welcome to the inaugural edition of The Appraisal, a monthly newsletter on real estate tech. I will focus my writing on the 30+ public companies operating at the intersection of real estate and technology. My hope is that this newsletter will provide readers with both an update on how these companies are performing, as well as broader insights across the venture capital, real estate, and mortgage ecosystems.

I also view this newsletter as a place to share my frameworks for assessing real estate technology businesses. As an investor at Thomvest Ventures focused on real estate technology, I’ve had the opportunity to meet with hundreds of entrepreneurs building special companies. Expect to see deep dives on specific companies or categories in this newsletter (see my Lemonade and Opendoor S-1 tear-downs for reference).

If you have any colleagues may find The Appraisal valuable, please feel free to share this newsletter. Thank you and enjoy!

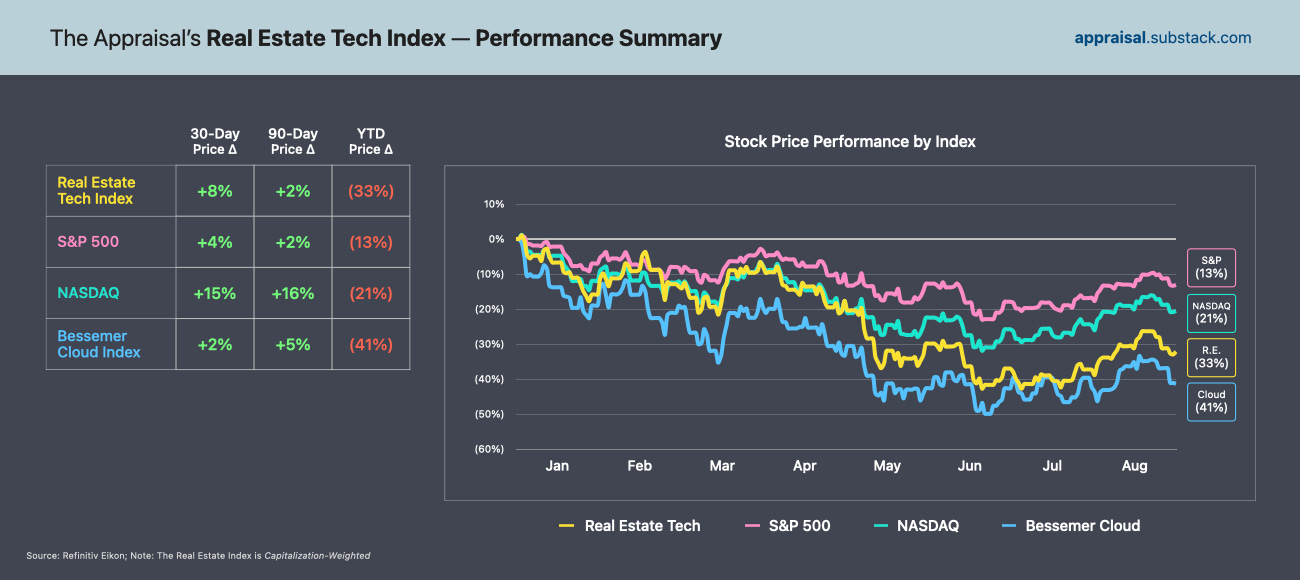

Highlight of the Month — The Real Estate Tech Index

I’ve organized 31 publicly-traded companies operating within the real estate sector into 7 distinct categories (see above). Many of these companies went public over the last two years during a flurry of IPO & SPAC activity. Unfortunately, the last several months have been extremely volatile for technology stocks — and real estate technology stocks in particular. Following rapid appreciation over the prior two years, the NASDAQ index is down 21% in 2022 and the real estate tech index is down 33% (the index is capitalization-weighted).

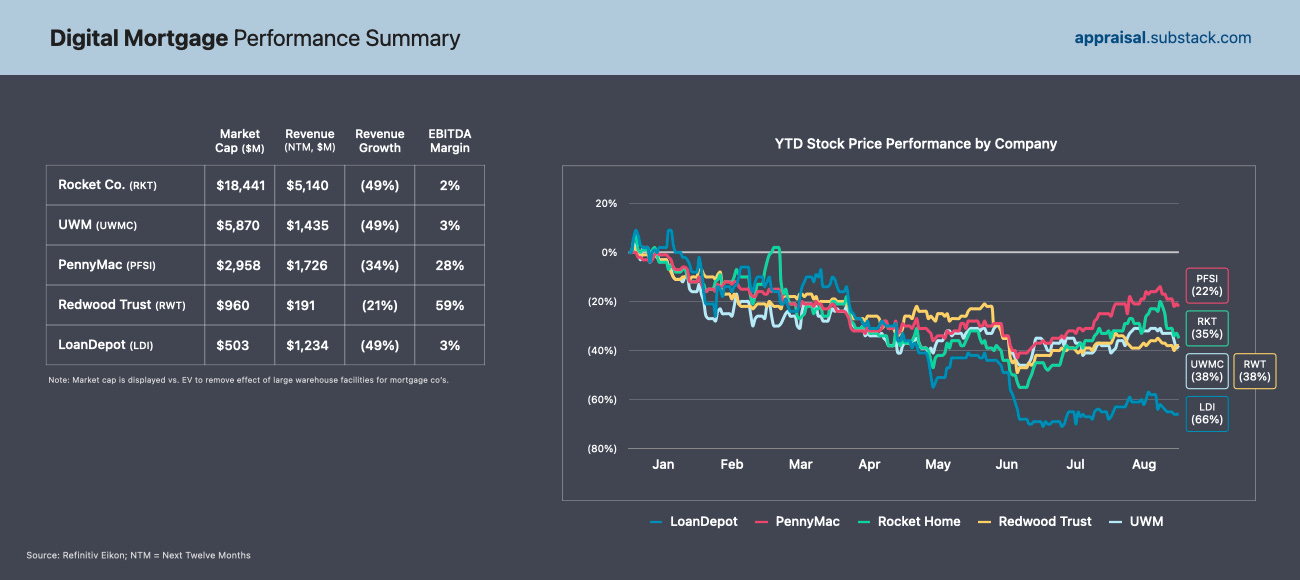

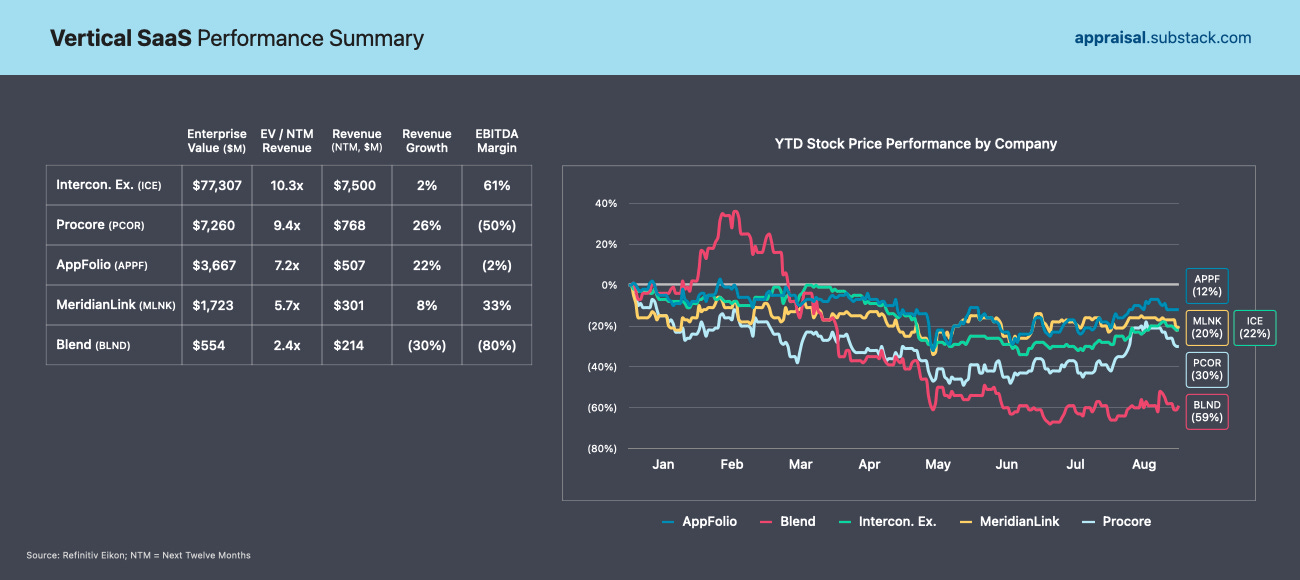

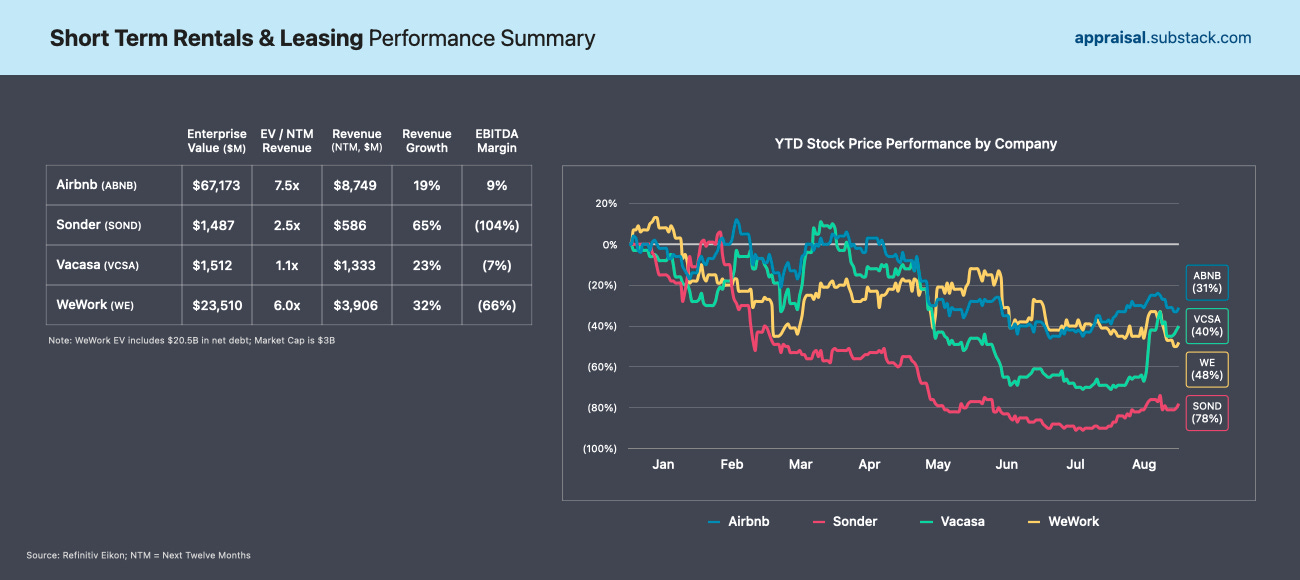

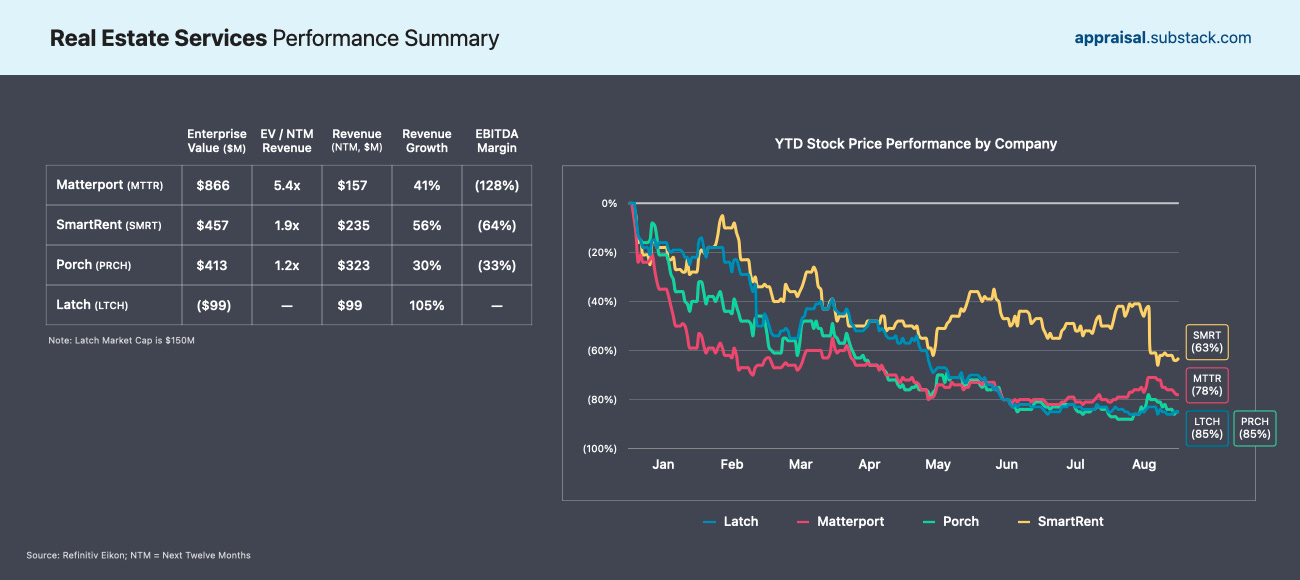

As you’ll see in the charts below, public real estate technology companies across every category have traded down meaningfully from their 2021 peak. High inflation and the Federal Reserve's decision to raise interest rates has spurred an exodus from tech stocks this year, especially those with higher valuations. Many technology companies in the real estate vertical are down by more than 50% in 2022, including Opendoor (-68%), Redfin (-76%), Sonder (-78%) and Latch (-85%).

This rising interest rate environment has had a particularly strong impact on real estate technology companies — resulting in a powerful one-two punch of 1) multiple contraction across all growth technology stocks and 2) softening housing demand resulting from elevated mortgage rates (median rates have nearly doubled from less than 3% to about 5.5% over the last year). Many real estate companies generate revenue on a transactional basis, meaning a softening housing market has a direct impact on revenue growth expectations.

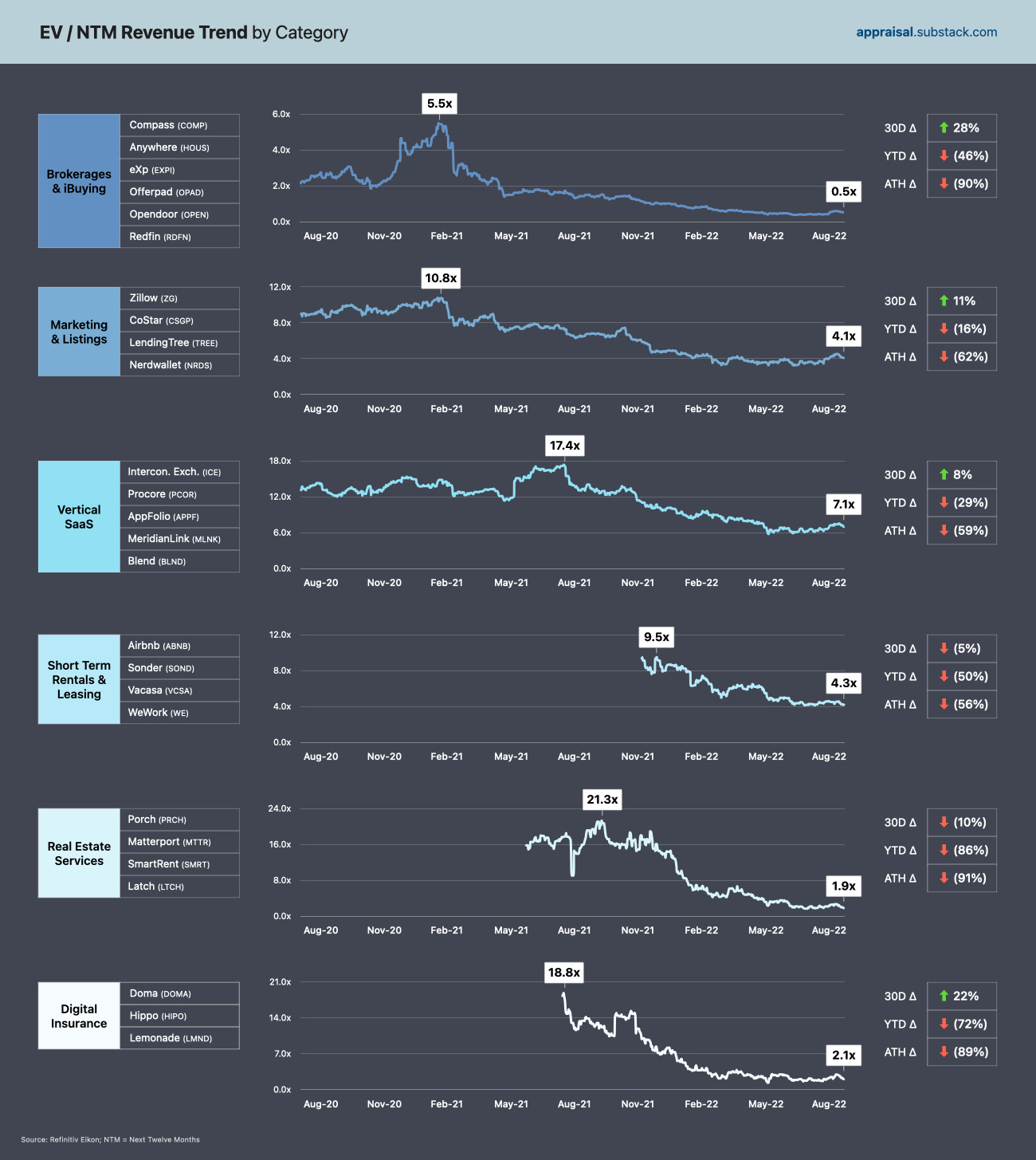

This has led to declining valuation multiples across every real estate segment. For example, the average EV (enterprise value) to NTM (next twelve months) revenue multiple in the Brokerages & iBuying segment has fallen from a peak of 5.5x to 0.5x as of August 2022. Similarly, valuation multiples within Digital Insurance segment have declined precipitously, from 18.8x in August 2021 to just 2.1x in August 2022 (see graphic below).

What can we attribute to declining valuations and worsening investor sentiment? In my view, there are three primary drivers:

Macro-environment: Concerns of a looming recession in the U.S. driven by rising interest rates, high inflation and declining GDP are impacting housing market outlooks over the short term, particularly after a decade-long bull market following the GFC. As mentioned above, this directly impacts short-term revenue outlooks amongst real estate technology companies.

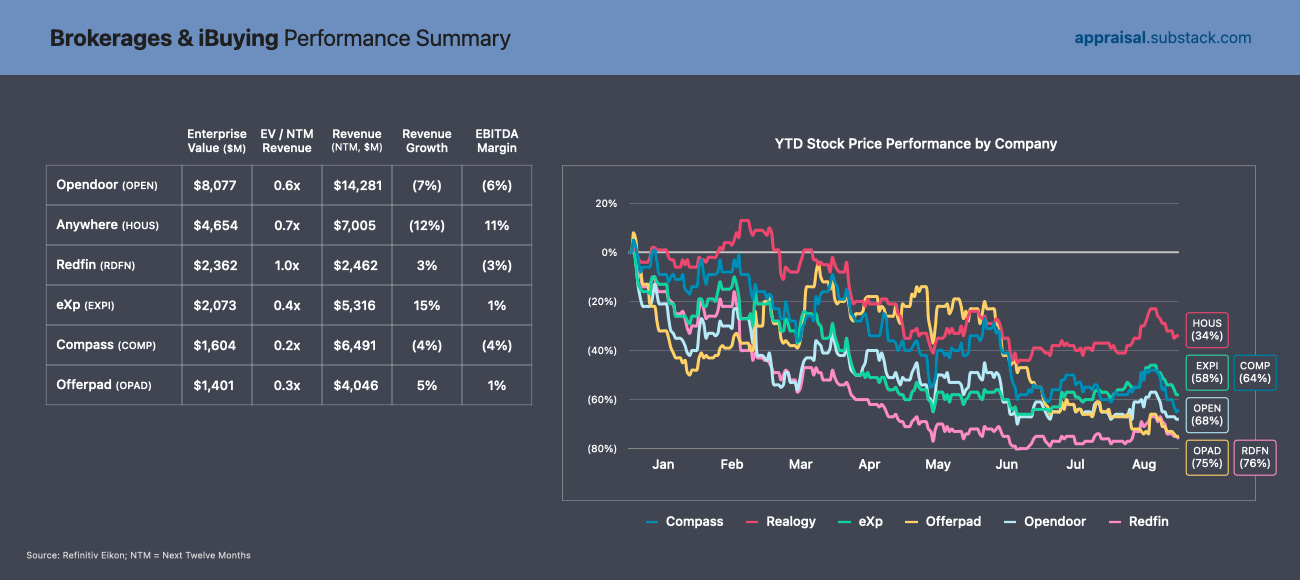

Newly public companies: 23 of the 31 companies included in this index went public in the last two years — and 15 of these companies went public via a SPAC merger. An argument can be made that these businesses have not reached the scale or revenue predictability to perform well as public, liquid stocks that are subject to heightened investor scrutiny. For example, smart lock maker Latch recently announced that its audit committee launched an investigation into the company’s “revenue recognition practices, including the accounting treatment, financial reporting and internal controls related thereto.” The company’s current market cap (~$150m) is less than its cash balance (~$250m) — a reflection of eroding investor confidence in the business.

Transition from growth to profitability: Public market investors have shifted from a weighting favoring top-line growth toward a greater focus on profitability. Many recently public companies in the real estate index have yet to achieve profitability. And investors fear that cash burn may materially worsen during a slowing housing market — for example, in its first year as a public company, Compass failed to generate profits during a period of record home price appreciation, and the company has had trouble convincing investors that it is on a path to profitability as US housing cools in 2022 (the stock is down 64% year-to-date).

So amidst this doom and gloom, where do we find silver linings? First, I continue to be a deep believer in the positive role technology plays in making real estate transactions more efficient, more data-driven, and more equitable. The long-term vision of these businesses remains compelling despite recent headwinds. The problems technology companies are solving are systemic in the real estate sector, and are relevant no matter the macroeconomic environment. Second, many companies recently announced cost-savings plans in an effort to assuage investor concerns around cash burn — and the real estate index has become slightly less volatile, up 5% over the last 90 days. Finally, I expect a period of heightened consolidation in the real estate category over the next several months given attractive entry prices relative to historical norms. Companies that are in a position to pursue an aggressive M&A strategy will be emboldened to do so, which may buoy multiples across real estate segments.

Below I’ve included category-level performance summaries. I will update the charts included in this newsletter on a monthly basis in order to track company & category performance over time. I am always open to feedback or thoughts on the newsletter — please feel free to respond to this email or shoot me a note at nima@thomvest.com.

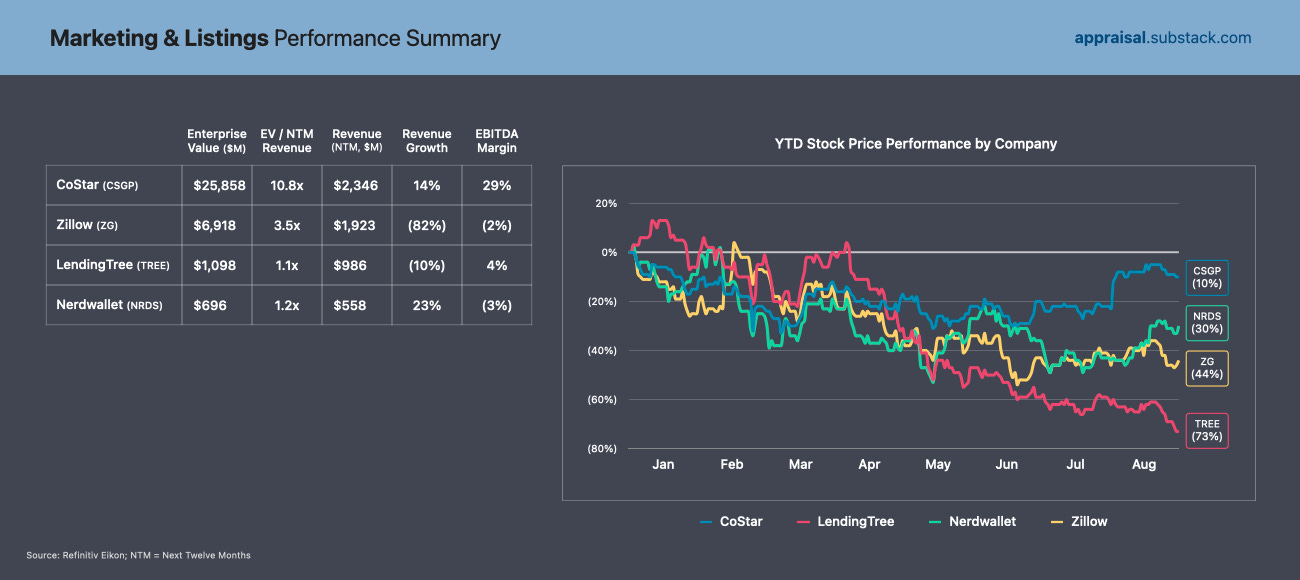

Public Real Estate Tech Performance Summaries

Note: Charts and graphs provided within are for informational purposes solely and should not be relied upon when making any investment decision. The content speaks only as of the date indicated. Any projections, estimates, forecasts, targets, prospects, and/or opinions expressed in these materials are subject to change without notice and may differ or be contrary to opinions expressed by others.

well written nima! are you switching from medium to substack? im excited to see your upcoming issue. have you seen https://www.mikedp.com ? his recent analysis on opendoor was great. would love to read your thoughts on where the industry is heading + trends you're seeing.