ServiceTitan S-1 Breakdown

This is a special edition of the newsletter — we’re breaking down ServiceTitan’s recent S-1 filing. Their IPO is a great win for the trade software category and the LA tech ecosystem. Enjoy!

ServiceTitan is a software company focused on creating tools for the trade professionals — plumbers, electricians, HVAC technicians, landscapers, and more. And it just announce its plan to IPO early next year. Let’s dig into the company’s S-1 filing.

While the trade industry is large, it has historically been underserved by technology. ServiceTitan's founders, Ara Mahdessian and Vahe Kuzoyan, are the sons of trade business owners, so they have a personal connection with the industry. They watched their parents struggle to do “the second job” of running the business after a long day in the field — paperwork, invoicing, and scheduling. Realizing that there was a gap in the market for technology to serve the trades, they founded ServiceTitan in 2007. The company has built an end-to-end cloud-based platform that helps tradespeople manage their business. The platform has the following capabilities:

Sales and Marketing: This includes features to help tradespeople generate leads, track leads, and manage their marketing campaigns.

Field Service Management: This includes features to help tradespeople schedule and dispatch technicians, track their progress, and manage their inventory.

Customer Relationship Management: This includes features to help tradespeople track their customer interactions, manage their contracts, and provide excellent customer service.

Human Capital Management: This includes features to help tradespeople manage their employee onboarding, payroll, and benefits.

FinTech: This includes features to help tradespeople process payments, offer financing, and manage their cash flow.

Through both organic product growth and a long history of acquiring adjacent software business, ServiceTitan has evolved into a broad platform for nearly every trade workflow — becoming the “operating system that powers trades.” This is a big platform in a big category — more than $1.5 trillion is spent annually on trades services in the United States and Canada.

Financial Profile

ServiceTitan's S-1 shows a company with solid growth, a sticky product, and improving profitability. The business has scaled meaningfully over the last 15+ years — trailing 12-month revenue is $685 million (as of July 31, 2024). Strong customer retention is highlighted as a key attribute of the business — net dollar retention rate was 110% or higher over the last 10 quarters, which demonstrates expanding usage over time. Revenue per active customer grew from $72K to $78K between 2023 and 2024.

Despite strong growth and retention, the company has yet to reach profitability, although it is closing in on the milestone. ServiceTitan grew 26% and had -25% FCF margins over the last 12 months, implying a “Rule of 40” value of 1% (TTM revenue growth + TTM FCF margin).

On a non-GAAP basis, ServiceTitan has reached operating profitability in its last three quarters (generating $15m in cumulative operating income over the last year), which will likely be highlighted on its roadshow as an early indicator of free cash flow generation.

The company has raised ample venture capital while private, including a $200 million Series G in 2021 that valued the company at $9.5 billion on a post-money basis, and a $365 million Series H in late 2022 that reset its valuation to $7.6 billion (post-money). On secondary markets, ServiceTitan shares currently trade around $80, slightly below its Series H price. That implies a valuation of about 10x current ARR, which is above the median EV / revenue multiple in Bessemer’s Cloud Index. We don’t yet have an indication of where the IPO will price.

Looking Forward

So what is ServiceTitan’s path to becoming a large and profitable company? Below I’ve outlined three key “things you need to believe” as the company marches down that path.

ServiceTitan will continue to acquire trades at scale, both via organic and inorganic acquisition

The company has done a good job growing its revenue base to more than 8,000 active customers while simultaneously driving down its sales and marketing expense relative to overall revenue. As of April 2024, S&M represented 30% of total revenue, down from 50% in early 2022. CAC payback appears to be quite strong as well, coming in at about 12 months last quarter. This is derived by dividing the previous quarter’s sales and marketing spend by the annualized gross margin added in the quarter. Less than one year is considered best in class among SaaS companies. The company also highlighted growing efficiency in its sales cycles in its S-1:

“We often sell to business owners and key executives, who know the needs of their business best, and understand the full breadth of pain points with existing solutions, and our deep domain expertise gives us the credibility to speak their language during the go-to-market process, leading to a sales cycle that, between January 1, 2024 and July 31, 2024, was on average less than 60 days.”

Acquisitions have also been an important component of ServiceTitan’s growth story, having made 10 acquisitions since 2018, according to Pitchbook. The company has utilized M&A to build a comprehensive platform (or “OS”) for trades, inclusive of every nearly software acronym out there — CRM (customer relationship management), CS (customer support), FSM (field service management), ERP (enterprise resource planning), HCM (human capital management) and FinTech (payments and lending). Recent acquisitions include:

Convex: Advanced CRM and data platform for commercial contractors. Acquired April 2024.

Schedule Engine: Appointment scheduling and management platform for home and commercial services. Acquired June 2022.

FieldRoutes: Leading FSM provider in the pest control and lawn care industries. Acquired January 2022.

ServicePro: Software for pest control companies, including inventory management, scheduling, reporting, intelligent routing. Acquired February 2021.

Aspire Software: Leading software provider for commercial landscaping businesses. Acquired June 2021.

I expect ServiceTitan to continue to flex its corporate development muscle as a public company, although it does specifically highlight acquisitions as a risk in its S-1:

“We have and may continue to pursue acquisitions to expand our business and operations. This rapid growth and organizational change have placed, and may continue to place, significant demands on our management and our operational and financial resources and could challenge our ability to develop and improve our operational, financial and management controls; enhance our reporting systems and procedures; recruit, train and retain highly skilled personnel; and maintain customer satisfaction.”

The AI opportunity in trades will accelerate ServiceTitan’s take rate and growth rate

ServiceTitan's platform is designed to be modular, allowing customers to start with a basic package and add more features as their business grows. Growing revenue per customer is a key component of the company’s strategy. The S-1 highlights this in its market opportunity definition:

“Based on our approximately $650 billion serviceable industry spend and our estimate that we have the opportunity to capture on average approximately 2% of our customers’ GTV as revenue, we estimate ServiceTitan has a serviceable market opportunity of approximately $13 billion.”

Today, the company captures 1% of gross transaction volume as revenue. Adoption of AI-related products will be critical in doubling that figure — ServiceTitan believes it is uniquely positioned to benefit from AI due to its access to a proprietary customer data, the similarity of its customer profiles, and its end-to-end platform. Currently, the company is using AI in two primary ways:

AI Features and Insights: The company is embedding AI-driven features and insights into its existing products. For example, ServiceTitan has developed an AI-powered document reader that can automatically extract data from invoices and other documents. The company has also developed an AI-powered dispatching tool that can help businesses optimize their routes and schedules.

AI Products: The company is also developing new, purpose-built AI products. For example, ServiceTitan recently launched a product called “Dispatch Pro,” which is an AI-driven dispatching and routing solution. The company plans to launch additional AI products in the future — think agents that manage key front- and back-office functions.

Examples of current AI-driven use cases include:

Smart Recommendations in Pricebook Pro: This feature uses AI to analyze historical data and provide pricing recommendations, enabling contractors to set competitive prices and maintain profitability.

Sales Pro: This AI-powered tool analyzes sales interactions and provides personalized coaching to technicians, helping them improve their sales techniques and close more deals.

Ads Optimizer in Marketing Pro: This tool utilizes AI to help businesses target the right customers for their advertising campaigns, improving the return on investment for their marketing spend.

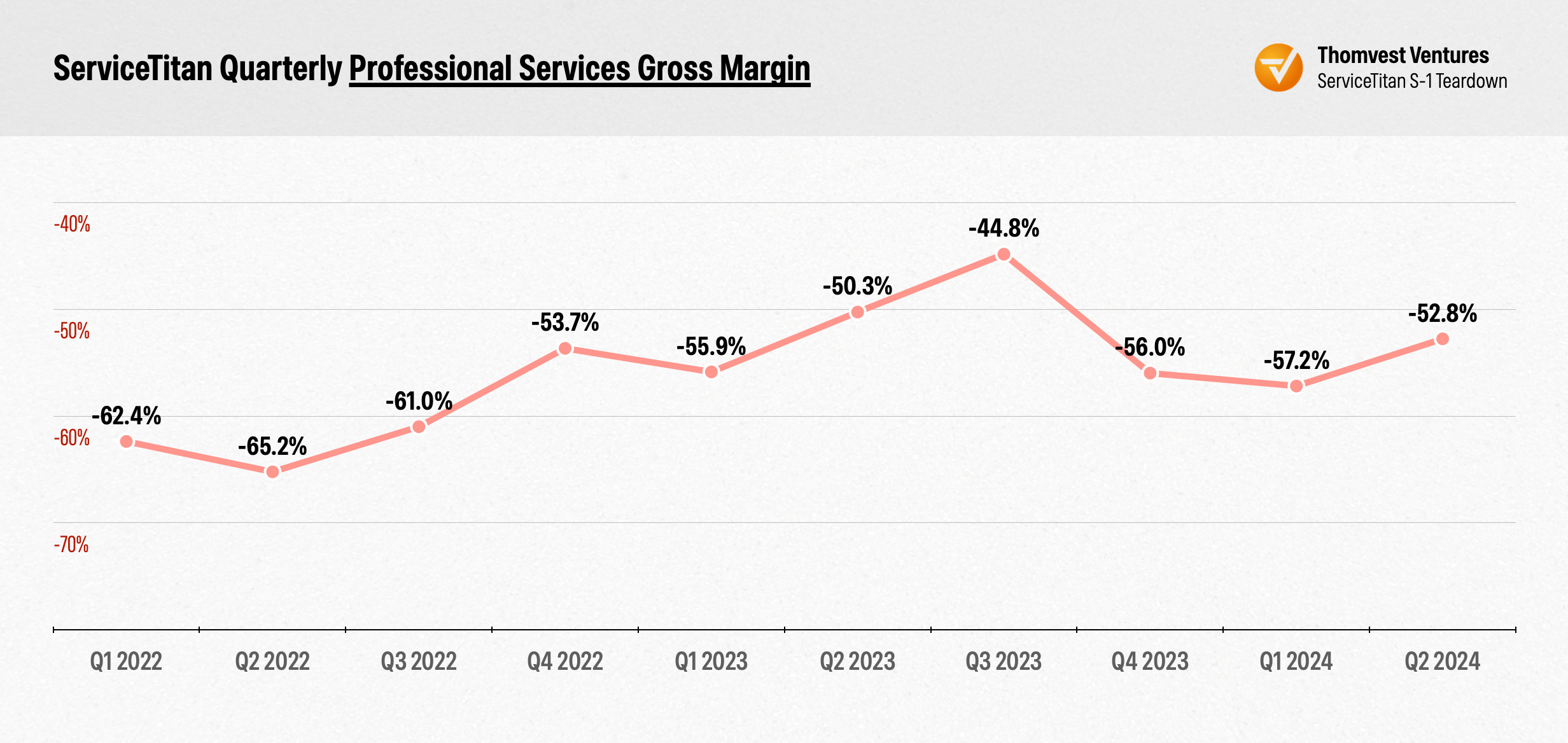

ServiceTitan will scale customer acquisition and onboarding without a heavy professional services cost

Professional services revenue, which comes primarily from onboarding, training, and other consulting services, is currently outweighed by the cost of providing these services. The company’s margin on professional services is -53% as of April 30, 2024, which drags down overall gross margin by nearly 8 points (73.4% platform gross margin vs. 65.7% overall gross margin).

The high cost of professional services is largely due to the labor-intensive nature of the onboarding and training process. Each new customer requires a significant investment of time and resources to get them up and running on the platform. SaaS investors are accustomed to higher gross margin (80%+) businesses — so expect the company to make progress on this metric post-IPO.

Other Highlights

ServiceTitan’s founders are retaining control of the business post-IPO via a multi-class share structure. The founders will hold class B stock (representing about 17% of fully total shares). Each share of Class B common stock is entitled to 10 votes. From the S-1:

“The multi-class structure of our common stock is intended to ensure that, for the foreseeable future, our Co-Founders continue to control or significantly influence the governance of the company, which we believe will permit us to continue to prioritize our long-term goals rather than short-term results, to enhance the likelihood of stability in the composition of our board of directors and its policies and to discourage certain types of transactions that may involve an actual or threatened acquisition of the company.”

According to the S-1, ServiceTitan has raised $1.4 billion since its founding. Bessemer Venture Partners (Series A lead), Iconiq Capital (Series B lead), and Battery Ventures (Series C lead), and Index Ventures (Series D lead) are the largest venture investors on the cap table.

Investors in the company’s Series F, G and H rounds are entitled to a conversion price adjustment in the event the initial public offering price is less than a pre-determined per-share value. Essentially, this anti-dilution provision protects investors in the case of a “down-round,” i.e. a per-share value at IPO that is less the per-share value from these prior rounds. From the S-1:

“If the Company’s IPO occurs after May 22, 2024 and is priced less than the conversion price of the Series H redeemable convertible preferred stock accreting at 11% per annum, accruing daily and compounding quarterly from and after May 22, 2024 (the “Ratchet Adjustment Denominator”) then the conversion price of the Series H redeemable convertible preferred stock is reduced to an amount equal to the product of (a) the IPO price, multiplied by (b) $84.5712 divided by the Ratchet Adjustment Denominator.”

The company shared details of its recent acquisition of Convex, sales and marketing platform built specifically for the commercial services industry. From the S-1:

“In April 2024, we acquired 100% of the outstanding equity of Convex Labs Inc., or Convex, a sales and marketing platform built specifically for trades businesses focused on serving commercial buildings that provides a comprehensive view of commercial properties, for a purchase price of $26.1 million, which consisted of 378,711 shares of our Class A common stock, valued at $23.8 million, in addition to $2.3 million in cash.”

The company highlighted LLMs as a risk factor in its prospectus, specifically mentioning the “risk that AI solutions could produce inaccurate or misleading content or other discriminatory or unexpected results or behaviors (e.g., LLM hallucinatory behavior that can generate irrelevant, nonsensical or factually incorrect results).” Additionally, the company acknowledge IP risk when utilizing LLMs: “Content, analyses or recommendations generated by our LLMs could produce information or other content that infringes, misappropriates or violates the intellectual property rights of others.”

Thanks for reading! As always, please feel free to share feedback or thoughts on this newsletter — you can respond to this email directly or shoot me a note at nima@thomvest.com.

Note: Charts and graphs provided within are for informational purposes solely and should not be relied upon when making any investment decision. The content speaks only as of the date indicated. Any projections, estimates, forecasts, targets, prospects, and/or opinions expressed in these materials are subject to change without notice and may differ or be contrary to opinions expressed by others.